Read the original publication (paywall)

The fight against the washing of dirty money began with good intentions in 1989. Three decades later it is judged to be a massive failure.

After working as a prudential regulator for 20 years in Australia and the Bahamas, Charles Littrell brings a unique perspective to the topic of money laundering and how to stop it.

He thinks the current anti-money-laundering (AML) regime, which centre on banks reporting millions of transactions each day at an annual compliance cost of perhaps $US300 billion ($432 billion), is a joke.

“It’s just an astounding policy failure,” he says in his first interview since returning to Australia after a five-year stint as Inspector of Banks and Trusts for the Central Bank of the Bahamas.

“The AML system we have is a child of the American war on drugs, which has been an utter failure except in one respect – it’s been a huge success as a war on black families. It exceptionally kicked the shit out of them.”

Littrell’s suggestion of racial bias in the enforcement of AML laws echoes a paper he published at the world’s biggest AML conference held in the Bahamas in January last year.

The paper, Biases in National AML Risk Assessment, concluded that dirty money in aggregate is much more of a problem in white majority countries and for major financial institutions in those countries, than in non-white countries.

Yet, his analysis shows that the Financial Action Task Force (FATF), which was established by the seven richest countries in 1989 to rein in AML, has assessment processes that display bias in favour of the United States, Australia, Canada and New Zealand.

Drowning in hypocrisy

He says the technical compliance assessment by FATF is not demonstrably biased against black majority jurisdictions, but the FATF effectiveness ratings are largely a function of whether or not the country in question is black majority and/or a small island state.

“America and the UK are the world’s two biggest arbiters of which countries are good or bad, but they are also the two biggest collective recipients and probably originators of dirty money,” he says. “And until they fix that basic problem, the whole system is just going to drown in its own hypocrisy.”

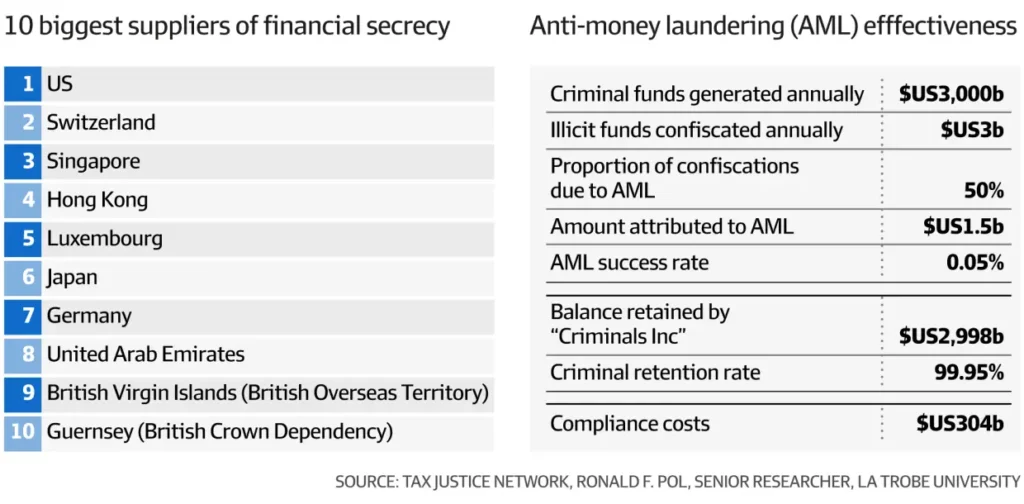

This analysis fits with the findings of the Tax Justice Network’s annual publication of the 10 countries most complicit in helping individuals to hide their wealth from the rule of law. The list is headed by the US.

To gain a more profound understanding of how the US facilitates money laundering, read the piece in The Guardian in November 2019 by British journalist Oliver Bullough on why the US state of South Dakota is the preferred tax haven for the super rich.

In the AML world, Bullough is one of the staunchest and most incisive critics of the FATF regulatory system. He has published two books: Moneyland, an exposé of offshore financing, and Butler to the World, a clear-eyed analysis of how Britain laid out the red carpet for oligarchs, kleptocrats and gangsters.

The FATF policy paradigm rests on two foundations: a know your customer requirement that forces people to fill in proof of identity forms; and the monitoring of billions of transactions run through financial institutions.

“One problem with the international AML framework is billions of honest people are inconvenienced or shut out of the system who are honest,” Littrell says.

“There’s zero evidence that crime is reduced as a result of all this AML. The best estimates say that over 99 per cent of the world’s cross-border, illicit funds is all happily proceeding along.

“So, we’re in a system where if you have a child who wants to go to Oxford University, that child will have more trouble opening a £5000 bank account with a British bank than a Russian kleptocrat would have putting £5 billion in the same British bank. What’s wrong with that picture?”

Littrell, who has been retained as consultant to the Bahamas Central Bank to run its annual AML conference for the next two years, was shocked at the outcome of the inquiries into large-scale money laundering through casinos at Crown Resorts and The Star.

When the money stops, someone buys a luxury mansion, someone invests in a trust, someone buys a suitcase full of $100 notes, or whatever – it’s just sitting there, and you can find it.

— Charles Littrell

“In our world, if someone commits fraud, they’re probably gonna go to prison, and if a company is said to be rotten, that company is gonna be closed or merged and the shareholders are gonna get hammered.

“But in Australian gaming, a casino licence means I only have to say, I’m sorry. I don’t actually have to do anything, or lose anything. And the state regulators will say to a casino owner: ‘Oh, you’ve been bad, you can have a licence, but please sell your business for $5 billion to the next guy’.”

He reckons there is a lot of merit in the findings of a controversial paper published in 2020 by Ronald Pol, who is a senior researcher at La Trobe University.

Pol argued that AML policy intervention has less than 0.1 per cent impact on criminal finances, compliance costs exceed recovered criminal funds more than 100 times over, and banks, taxpayers and ordinary citizens are penalised more than criminal enterprises.

Littrell says that although many disagree with some of the calculations and analysis in Pol’s paper, there is a strong consensus that there is a yawning gap between criminal funds generated annually and the AML success rate.

Lack of questioning of the regulatory paradigm is a function of the incentives in the AML ecosystem for hundreds of thousands of businesses and professionals, according to Pol’s paper.

“Banks must also avoid or mitigate regulatory sanction, which means implementing AML programs and complying with laws dictated by standards framed in the global policy prescription,” Pol’s paper says.

“In a compliance-oriented intervention model, if such laws achieve their policy objective, or not, is immaterial. Banks and other firms must comply, or risk ruinous reputational damage and financial penalties.”

Littrell is scathing in his criticism of Australia’s AML enforcer, AUSTRAC. He says that if the media reports are accurate, it was missing in action throughout the Crown and Star money laundering, which included bags of cash passing around and the use of credit card expenses to wash illicit gambling funds from China.

Also, he says the AUSTRAC action against Westpac in 2020 for breaches of AML laws was “the most chickenshit global AML enforcement I have seen anywhere”.

Littrell says reform of AML regulation requires four things: a switch in focus from monitoring transactions to finding out where the money is landing; removing the use of currency notes for illicit purposes; forcing the disclosure of beneficial interests behind trust corporations, foundations and shell companies; and making a clear distinction between financial crime and terrorism financing.

“When the money stops, someone buys a luxury mansion, someone invests in a trust, someone buys a suitcase full of $100 notes, or whatever – it’s just sitting there, and you can find it,” he says.

“Redirect your effort to focus on illicit assets starting with currency notes – 80 per cent of the value of US currency is in $100 notes. If you go to America, you never see them. But they turn out close to $150 billion a year of $100 notes, it’s their most lucrative export.

“If America and Europe and Canada and Australia and all these places withdrew their large denomination notes from circulation, let’s call it $2 trillion or $3 trillion worth of assets, of which probably more than half is illicit.

“Let’s not talk about financial crime as one big thing – it is not true. Terrorist spending is very different from drug dealer spending.

“Drug dealers commit a crime and then try to invest the money in legal things. Terrorists take legal money, typically, and try to spend it on illegal things, and in very different amounts and patterns of distribution.

“But they’re all lumped together in the same financial crime basket. They are not at all the same thing.”

Note: Following publication of this column, Littrell wrote an opinion piece for the Financial Review.